Private Hospital Prices Soar 47% Faster Than Medicare Rates Since 2019, KFF Analysis Reveals

New analysis reveals hospital prices for private insurance skyrocketed 47% faster than Medicare rates from 2019 to 2026, impacting healthcare affordability.

Healthcare costs continue to be a primary concern for the public, prompting a growing focus among policymakers on enhancing affordability. Hospitals command a substantial portion of overall healthcare expenditures, accounting for nearly one-third of total spending and contributing 40% to spending growth between 2022 and 2024. This trend in hospital spending is influenced by both the rates charged for services and the volume and intensity of care delivered, with implications for economic accessibility and expenditure increases.

Unprecedented Disparity in Price Growth

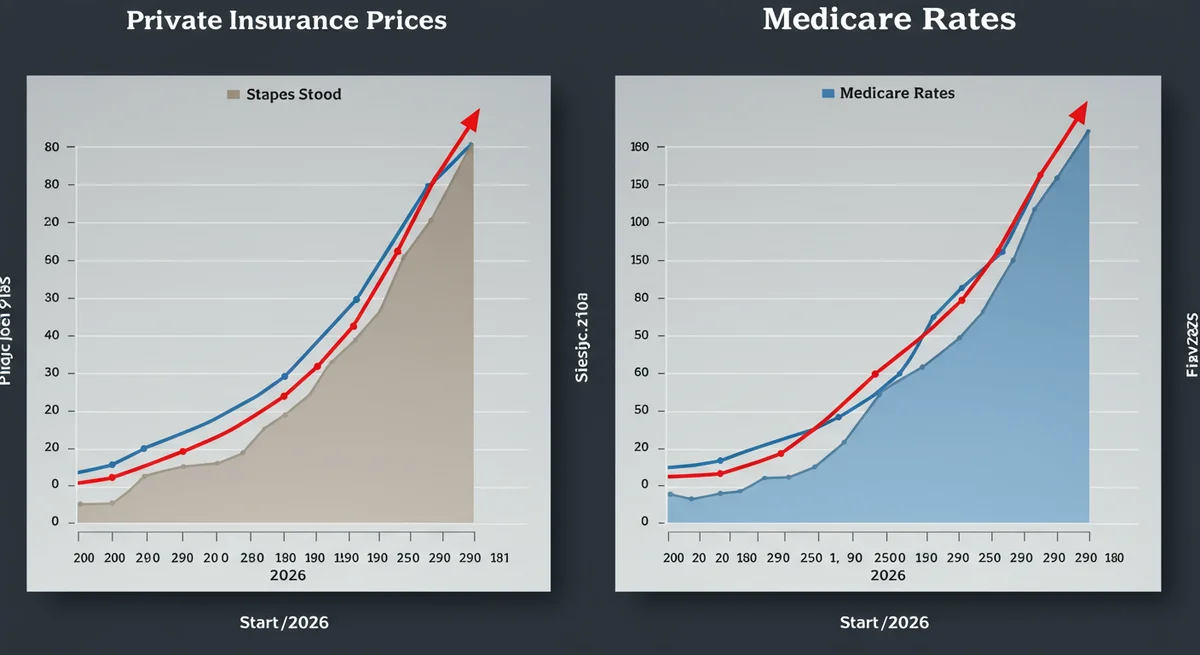

A recent analysis, drawing on data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI), highlights a significant divergence in hospital price escalation between private insurance and Medicare. From April 2019 through April 2026, private insurance rates for hospital care are projected to have climbed by 30%, a notable contrast to the 21% increase observed in Medicare rates over the identical seven-year period. This translates to private insurance prices advancing 47% more rapidly than Medicare rates.

Initially, from April 2019 to April 2020, both private insurance and Medicare rates progressed at a comparable pace. However, the period between April 2020 and April 2025 witnessed private insurance prices growing at an accelerated rate compared to Medicare. A slight reversal is anticipated from April 2025 to April 2026, with private rates increasing less quickly than Medicare. These patterns are generally consistent with prior studies that have identified quicker price growth for private coverage compared to Medicare over extended periods, although with some temporal variations. Earlier research already indicated that private plans typically pay substantially higher rates for hospital services than Medicare, and this recent analysis suggests that the gap has only widened.

Driving Factors Behind Private Rate Hikes

Private insurance hospital prices are fundamentally shaped by negotiations between healthcare facilities and insurers. The upward trajectory in these private rates can be attributed to several elements, including evolving costs for providing care and shifts in the negotiating power balance between hospitals and insurance providers. A key contributor to this trend is the increasing consolidation within hospital markets; by 2024, in a vast majority of metropolitan areas (83%), one or two health systems commanded at least 75% of the inpatient hospital care market, according to various analyses. This consolidation has been shown to result in higher prices.

Furthermore, substantial increases in labor and supply expenses experienced during the pandemic likely compelled providers to seek higher reimbursements. Economy-wide inflation notably surged in March and April 2021, peaking in June 2022. However, hospital-insurer contracts are typically renegotiated periodically and often span several years. This contractual structure can introduce a delay, meaning the full impact of elevated input costs may not immediately reflect in higher prices.

Medicare's Regulated Rate Adjustments and Restraints

In stark contrast, traditional Medicare hospital prices undergo annual adjustments by the Centers for Medicare and Medicaid Services (CMS), primarily through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS). These modifications are determined by factors and methodologies stipulated in legislation and regulations. IPPS and OPPS updates are partly based on projections of increases in hospital services' input costs, which are themselves influenced by broader inflation trends. Evidence suggests that rates paid by Medicare Advantage plans for hospital services generally align closely with those of traditional Medicare. Increases in prices paid by Medicare Advantage insurers have likely followed traditional Medicare rate changes over time.

Several elements have contributed to a more tempered growth in Medicare rates during the study period. One such factor is the program's occasional underestimation of inflation when prospectively setting rates, as noted by the hospital industry and other observers (e.g., 2022 inflation significantly exceeded expectations during that year's rate-setting). Despite this, CMS has indicated that its forecasts for the IPPS hospital market basket have, on average, closely mirrored actual inflation over longer durations.

Additional restraints on Medicare price growth include productivity adjustments mandated by the Affordable Care Act, which are designed to reduce the growth of traditional Medicare rates over time under the assumption of increased hospital efficiency. Sequestration, an automatic reduction in Medicare payments required by budget rules, also played a role; it was temporarily suspended during the pandemic beginning in May 2020 but gradually reinstated in April and July 2022, influencing the Medicare PPI's fluctuations during those periods.

Policy Interventions and Data Methodology

Discussions at both national and state levels are exploring policy avenues to curb hospital prices. One approach advocates for fostering competition and mitigating consolidation within provider markets, as extensive research links hospital market consolidation to elevated prices without clear evidence of improved service quality. Another strategy involves direct price regulation, such as imposing caps on what providers can charge. For instance, Indiana recently enacted legislation to eventually cap private insurance prices for the state's non-profit hospitals. Oregon has maintained a cap on hospital prices at 200 percent of traditional Medicare rates for its state employee plan since 2019.

This analysis relied on the Producer Price Index (PPI) from the BLS to assess hospital prices and overall inflation over the seven-year period from April 2019 to April 2026. The PPI measures prices from the perspective of service producers, such as hospitals. It was preferred over alternative measures like the Consumer Price Index (CPI) because of its capacity to disaggregate hospital price growth by payer type, specifically Medicare and private insurance. The PPI for private insurance excludes private Medicaid and Medicare plans, while the Medicare PPI encompasses both traditional Medicare and private Medicare plans, including Medicare Advantage, which covered 54% of the eligible Medicare population in 2025.

Most observed increases in the Medicare hospital PPI typically occur in October and January, largely reflecting the timing of when traditional Medicare updates inpatient and outpatient reimbursement rates for hospitals, respectively. CMS, in its FY2026 IPPS rule, reiterated the long-term accuracy of its IPPS hospital market basket forecasts. While comments, including from the hospital industry, were submitted during the 2026 rulemaking process advocating for higher IPPS operating and OPPS payment rates to compensate for past forecasting inaccuracies, CMS did not implement these changes, citing various reasons. Adjustments for forecasting errors are made for IPPS capital payments, which constitute a smaller share of total hospital payments.

Latest Updates on this Story

As the healthcare landscape continues to evolve, stakeholders are closely monitoring legislative actions and economic shifts that could further impact hospital pricing trends. Breaking news and ongoing analyses will provide crucial insights into how these disparities influence patient costs and health system stability. You can monitor all live updates on this story in real-time on MedicareTicker.com.

Related Topics

🔹 Medicare Costs 🔹 Private Health Insurance 🔹 Hospital Pricing 🔹 Healthcare Affordability 🔹 CMS Regulations 🔹 Market Consolidation 🔹 Producer Price Index

About MedicareTicker News

MedicareTicker.com provides unparalleled coverage and in-depth analysis of healthcare costs and policy changes, with a particular focus on their impact on Medicare beneficiaries and the broader insurance market. We serve as the leading independent resource for current news, trends, and expert insights within this critical domain, helping our readers navigate the complexities of the healthcare system.

Frequently Asked Questions

Why have private insurance hospital prices grown faster than Medicare rates?

This disparity is attributed to several factors including increased hospital market consolidation, which enhances hospitals' bargaining power, and the lag in private insurance contract renegotiations reflecting rising input costs like labor and supplies.

What period does this analysis cover and what were the exact increases?

The analysis spans from April 2019 to April 2026. During this time, private insurance hospital prices climbed by 30%, while Medicare rates saw a 21% increase.

How do policy efforts aim to control hospital prices?

Policy discussions involve promoting market competition, regulating consolidation, and implementing direct price caps. Examples include Indiana's new law for non-profit hospitals and Oregon's 200% cap on Medicare rates for state employee plans.

What data source was used for this report?

This report utilized data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI), specifically chosen for its ability to differentiate hospital price growth by payer type, including Medicare and private insurance.