Medicare's Hidden Burden: Millions Face Steep Healthcare Costs Despite Coverage

New analysis reveals millions of Medicare beneficiaries struggle with healthcare affordability, facing high out-of-pocket costs, medical debt, and uncovered services. Learn the facts.

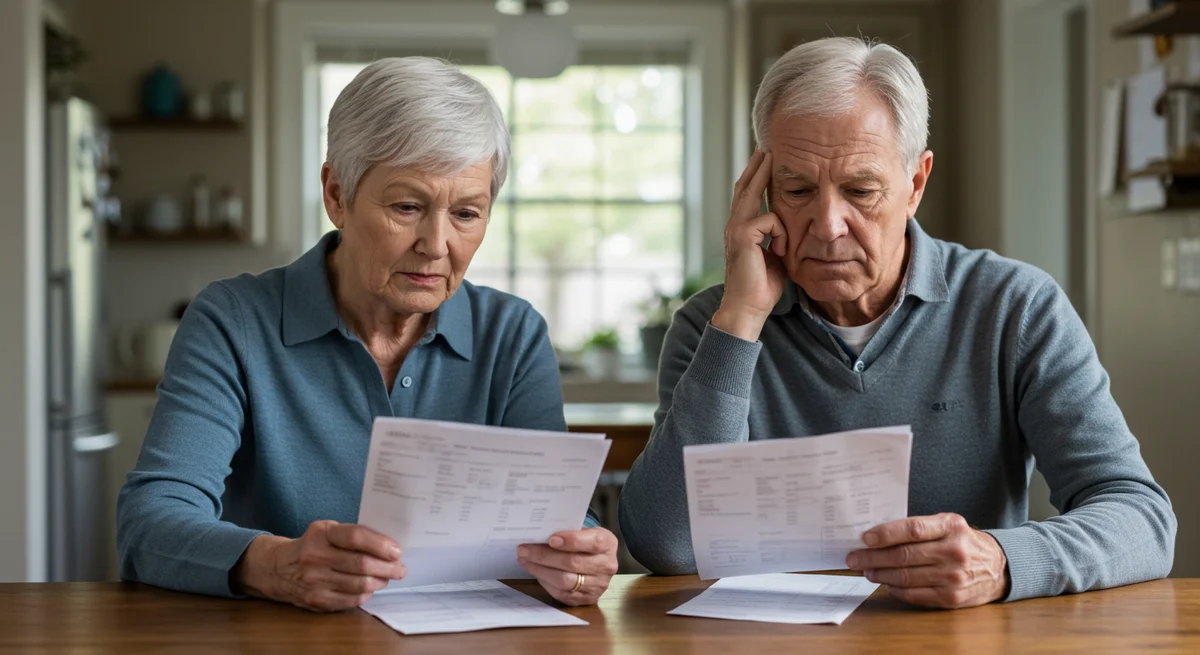

In recent public opinion surveys, the cost of healthcare and its affordability have emerged as a primary financial concern for individuals across the United States. Even insured populations report difficulties managing these expenses, a challenge that extends to those enrolled in Medicare. While Medicare extends health insurance benefits to approximately 70 million individuals, including those aged 65 and older and younger adults with enduring disabilities, possessing this coverage does not insulate beneficiaries from significant financial pressures related to medical care. Such pressures manifest as deferring necessary medical treatment due to cost or accumulating medical debt. A 2026 Health Tracking Poll indicated that nearly half (49%) of all Medicare beneficiaries aged 65 and older anticipate their healthcare expenditures will become even less affordable over the coming year.

This brief offers a detailed examination of healthcare affordability for Medicare beneficiaries, encompassing younger adults with long-term disabilities, drawing upon extensive data from diverse sources.

Financial Vulnerabilities Among Many Beneficiaries

A significant segment of the Medicare population lives on limited incomes and possesses modest savings, complicating their ability to pay for medical care and long-term support services. Data from 2024 shows that one in four Medicare beneficiaries, totaling 16.5 million people, had an annual income below $24,600, which represents approximately 160% of the federal poverty level for that year. These figures incorporate various income streams, including Social Security, pensions, and retirement account (IRA) withdrawals. Conversely, the wealthiest 5% of Medicare beneficiaries, about 3.3 million individuals, reported incomes exceeding $169,700 per person.

Many beneficiaries also hold relatively low levels of savings; in 2024, one in four had less than $18,950 in savings. Financial resources are even more constrained within specific demographic groups. For example, one in four Black beneficiaries earned less than $20,150 per person in 2024, while one in four Hispanic beneficiaries had incomes below $14,150 per person.

In 2024, roughly 6 million individuals aged 65 and older, or 10% of this demographic, lived in poverty according to the official poverty measure, meaning their income was $15,050 or less if single. An even larger proportion, 17.3 million (28%), had incomes below 200% of the poverty line. When assessed by the supplemental poverty measure (SPM), which accounts for higher out-of-pocket medical expenses among older adults, the poverty rate for seniors in 2024 climbed to 15%.

Dependence on Social Security income is substantial for many. In 2025, nearly a quarter (23%) of all Medicare beneficiaries receiving Social Security benefits relied on this income source for 90% or more of their total per capita earnings. About one-third (32%) depended on Social Security for at least 75% of their income. For those relying on Social Security for at least 90% of their income, the average per capita Social Security income in 2025 was $20,168. This figure was $20,670 for individuals relying on Social Security for at least 75% of their income.

Out-of-Pocket Burdens and Premium Pressures

Medicare premiums and other direct healthcare expenses consume a substantial portion of beneficiaries' incomes and household budgets. In 2023, out-of-pocket spending on health care, including premiums, represented 36% of the average Social Security income per person for Medicare beneficiaries. On average, beneficiaries spent $6,459 out-of-pocket on healthcare costs in 2023, while their average Social Security income stood at $17,718. It's important to note that most older adults have additional income sources beyond Social Security that can be used to cover these costs. Out-of-pocket expenditures also encompass premiums for supplemental coverage like Medigap, purchased by those in Traditional Medicare.

Healthcare spending constituted 14% of total household spending for Medicare households in 2024, a significantly larger share compared to non-Medicare households, which allocated 6% of their total household spending to health care in the same year.

For more than 7 million Medicare beneficiaries enrolled in Medicare Part B in 2024, premiums alone accounted for over 10% of their annual per capita income. The standard Part B premium, paid by enrollees in both Traditional Medicare and Medicare Advantage, has nearly doubled over the past decade, increasing from an annual cost of $1,259 in 2015 to $2,435 projected for 2026.

Cost Implications: Traditional Medicare vs. Medicare Advantage

The choice between Traditional Medicare and Medicare Advantage plans carries distinct financial implications. Traditional Medicare does not impose an upper limit on out-of-pocket spending for Medicare-covered hospital and physician services. In contrast, Medicare Advantage plans are legally mandated to include an out-of-pocket maximum for these services. In 2025, the average out-of-pocket limit for Medicare Advantage enrollees was $5,320 for in-network services and $9,547 for combined in-network and out-of-network services. The maximum permissible limits were $9,350 for in-network services and $14,000 for combined services in 2025, adjusting to $9,250 and $13,900, respectively, in 2026. While this cap shields Medicare Advantage enrollees from unlimited costs for covered services, cost-sharing requirements can still lead to substantial expenses before reaching the annual limit. Typically, Medicare Advantage enrollees do not pay an additional premium for the plan itself.

Medicare Advantage plans have the flexibility to reduce cost-sharing, offer benefits not covered by Traditional Medicare (such as dental and vision), and lower Part B and Part D premiums. This is facilitated by additional payments, known as rebates, they receive from the federal government beyond the standard cost of providing Part A and Part B services. In 2026, these rebates averaged approximately $2,660 per person. For services covered under Medicare Parts A and B, Medicare Advantage plans can structure cost-sharing differently than Traditional Medicare, often reducing it, and are prohibited from charging more for specific services like Skilled Nursing Facility (SNF) stays. Plans must provide coverage that is at least as comprehensive as Traditional Medicare overall, though out-of-pocket expenses can fluctuate based on the plan type, service utilization, and provider network participation.

Medigap policies offer a means for Traditional Medicare beneficiaries to limit their exposure to out-of-pocket medical costs, with the most popular plans covering nearly all cost-sharing for Medicare-covered services. However, Medigap underwriting rules can make these policies difficult or impossible for beneficiaries with pre-existing conditions to acquire outside of specific, limited enrollment periods. For those with modest incomes, the average monthly Medigap premium of $217 in 2023 could be financially prohibitive.

More than 3 million Medicare beneficiaries in Traditional Medicare lack any additional coverage, such as Medigap, employer coverage, or Medicaid, to assist with Medicare cost-sharing requirements. This absence of supplemental coverage leaves them vulnerable to high out-of-pocket costs if they require extensive or high-cost medical services, given the unlimited out-of-pocket spending for Parts A and B in Traditional Medicare.

Uncovered Services and Medical Debt: A Significant Burden

Beneficiaries often face substantial out-of-pocket costs for services not covered by Traditional Medicare, including dental, hearing, and vision care. In 2023, Traditional Medicare beneficiaries spent an average of $1,107 on dental services and $564 on hearing services. While most Medicare Advantage plans incorporate dental, hearing, and vision benefits, enrollees in these plans still incur out-of-pocket costs, averaging $571 for dental services and $212 for hearing services.

A 2022 report indicated that approximately one in five (22%) Medicare-age adults carried some form of debt from medical or dental bills. Among older adults with medical debt, about 40% reported reducing other household spending and depleting most or all of their savings due to these healthcare-related financial obligations.

Long-term services and supports (LTSS), which Medicare does not cover, remain unaffordable for all but the highest-income Medicare beneficiaries. In 2025, the median annual costs for common LTSS in the U.S. were $80,080 for full-time non-medical caregiver services (e.g., home health aide for daily living assistance), $129,575 for a private nursing home room, and $305,760 for round-the-clock home health aide services. These figures vastly exceed the median income ($43,200) and savings ($110,100) among the Medicare population. Generally, Medicare, whether Traditional or Advantage, does not cover long-term care services.

Medicaid's Crucial Role in Affordability

Medicaid plays a vital role in making Medicare affordable for approximately 12 million low-income Medicare beneficiaries, referred to as “dual-eligible individuals,” who also have Medicaid coverage in 2025.

Over seven out of ten (72%) dual-eligible individuals, totaling 8.5 million people, qualify for the full spectrum of Medicaid benefits not covered by Medicare. This includes long-term services and supports, vision and dental care, and non-emergency medical transportation (often called wraparound services). These “full-benefit” dual-eligible individuals typically also receive additional assistance through the Medicare Savings Programs (MSPs), which cover Medicare premiums and, in most cases, cost-sharing for individuals with limited income and assets.

The remaining 3.4 million dual-eligible individuals, categorized as “partial-benefit” individuals, do not receive comprehensive Medicaid benefits but do receive payments to cover Medicare premiums and, usually, cost-sharing through the Medicare Savings Programs. Federal guidelines stipulate that Medicare beneficiaries with incomes up to 135% of the federal poverty line and assets below specified levels ($9,950 for an individual and $14,910 for a couple in 2026) are eligible for financial aid from their state Medicaid program via an MSP. States have the option to cover Medicare beneficiaries with incomes or assets exceeding these federal limits, and 18 states chose to do so in 2026. Without financial support from Medicaid, the Part B premium alone would consume 15% of the income for a dual-eligible individual with a monthly income of $1,350, not accounting for other out-of-pocket expenses.

Prescription Drug Costs Remain a Concern

Medicare Part D provides a safeguard against exorbitant prescription drug costs, but these expenses continue to be a worry for older adults. Almost all Medicare beneficiaries (96%) utilize prescription medications, and the majority are enrolled in Medicare Part D drug plans for coverage. In 2023, Part D enrollees who did not receive low-income subsidies incurred average out-of-pocket prescription drug costs of $872. For those in fair or poor health, this average was nearly double, at $1,671.

The Part D low-income subsidy (LIS) offers significant financial assistance to individuals with incomes below 150% of poverty (under $23,940 for an individual in 2026) and limited assets (under $18,090 for an individual). In 2023, Part D enrollees receiving LIS had average out-of-pocket drug costs of $156, roughly one-fifth of the amount paid by others.

Latest Updates on this Story

As the debate around healthcare costs and senior financial security continues, breaking news indicates ongoing discussions in Congress regarding potential adjustments to Medicare's structure and benefit offerings to address these persistent affordability issues. Stakeholders are closely watching for any legislative proposals or regulatory changes that could impact millions of beneficiaries. You can monitor all live updates on this story in real-time on MedicareTicker.com.

Related Topics

🔹 Medicare Affordability 🔹 Healthcare Costs for Seniors 🔹 Medicare Advantage Plans 🔹 Traditional Medicare Expenses 🔹 Long-Term Care Funding 🔹 Medical Debt Crisis 🔹 Medicare Savings Programs

About MedicareTicker News

MedicareTicker.com provides comprehensive, independent news and analysis on all facets of Medicare, from policy changes and benefit comparisons to financial impacts and beneficiary experiences. As the leading independent resource in this domain, our coverage helps millions of Americans navigate the complexities of their healthcare choices.

Frequently Asked Questions

Why do Medicare beneficiaries still face high healthcare costs?

Despite having Medicare coverage, beneficiaries can incur significant out-of-pocket expenses from premiums, deductibles, co-insurance, and services not covered by Medicare, such as most dental, vision, and long-term care.

What is the difference in out-of-pocket limits between Traditional Medicare and Medicare Advantage?

Traditional Medicare does not have an annual out-of-pocket spending limit for covered services, leaving beneficiaries vulnerable to high costs. Medicare Advantage plans, by law, include an annual out-of-pocket maximum, which was, for instance, up to $9,350 for in-network services in 2025.

How does Medicaid help low-income Medicare beneficiaries?

Medicaid provides crucial support to low-income Medicare beneficiaries (dual-eligibles) by covering Medicare premiums, cost-sharing, and services not typically covered by Medicare, such as long-term care and some dental/vision benefits, through programs like Medicare Savings Programs.

What are the challenges in affording long-term care for Medicare beneficiaries?

Long-term services and supports (LTSS) are generally not covered by Medicare, leading to extremely high out-of-pocket costs that often far exceed the median income and savings of most beneficiaries, making it a significant financial burden.